Search

Recent comments

- not good advert....

1 hour 54 min ago - laws....

1 hour 59 min ago - firewave....

2 hours 31 min ago - another settlement....

3 hours 3 min ago - pro-war prostitutes....

3 hours 37 min ago - graylight....

19 hours 59 min ago - six elements?....

21 hours 24 min ago - liberating....

23 hours 26 min ago - burnt roast....

23 hours 55 min ago - no KA32....

1 day 55 sec ago

Democracy Links

Member's Off-site Blogs

liberal party connections lead the top ranks of nine news network.....

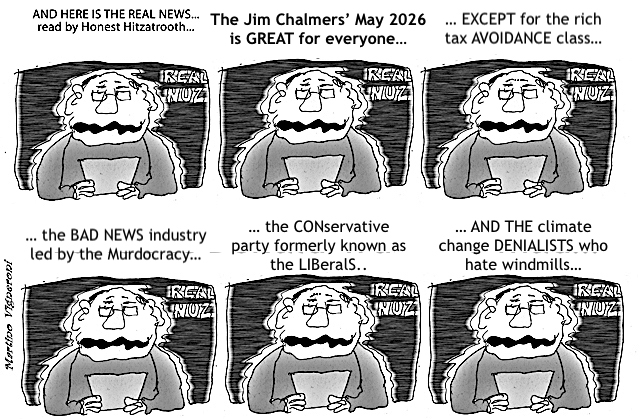

The media campaign against the Federal Budget is unprecedented, not for its vehemence but it’s uniformity across Murdoch and Nine Entertainment organs. Michael Pascoe fears for the future.

Peter Tonagh, the chairman of Nine Entertainment, is a former CEO of News Corp Australia. He is one of the four Nine board members who have Murdoch links. One of the remaining two was a senior advisor to Simon Birmingham when he was a Liberal Cabinet minister.

There’s a bit of that Liberal connection around the top ranks of Nine. The company’s director of communications and public affairs was a senior press secretary for Prime Minister Tony Abbott. The Australian Financial Review’s editor-in-chief, James Chessell, was a press secretary for Treasurer Joe Hockey.

Nine’s two top editorial executives – the managing director, publishing, and executive editor of the Sydney Morning Herald and the Age – are ex-News Corp, as is its director of streaming and broadcasting. Chessell and the Sydney Morning Herald editor both had stints in Murdoch newsrooms earlier in their careers.

Not that there’s necessarily anything wrong with that. Our very own Michael West won a Walkley Award for business journalism while at the Australian between posts at the AFR and SMH. Heck, I started on The Courier-Mail, but that was long before Murdoch got hold of it.

What has stood out, though, in the past two weeks is the similarity of the Murdoch and Nine campaigns. Has it been warranted, or is there a growing uniformity of culture in Australia’s two biggest media companies? In short, has there been a Murdochification of the former Fairfax?

Merger on the cards?The dismal reality of news media economics in general and Nine’s particular challenges as it struggles for corporate clarity suggest the outrageous possibility that the two are on a path to eventually be folded into each other. No prize for guessing which would fold around the other.

Nine and News already share printing and distribution. In the never-ending search for costs to be cut, an ownership-agnostic Nine board with no printer’s ink in its veins could well look at how much of their back offices are needlessly duplicated, how many other resources could be shared. You know, it’s all just content in the end, just different brands. And you know Albo would let them.

The increasingly common culture was displayed by the ABC’s MediaWatch on Monday night as it paraded the fishwrappers’ hyperbolic budget reactions with the AFR and SMAge (also known as “this masthead”) fitting in neatly amongst the Murdoch rags.

The AFR has been reduced to trolling readers for reactions, none better than its (fake) fleeing yarn.

MediaWatch could have gone much further if time had permitted, the media swallowing and repeatedly repeating the Coalition’s “Death Tax” furphy a case study in itself.

Of course, bad news sells, but time and again dodgy claims were headlined across Murdoch and Nine papers, the only difference being that Nine tended to include Treasury rebuttals, albeit at the end of the stories relatively few read, while Murdoch’s tabloids don’t bother.

My personal favourite was the AFR prominently headlining the opinion of a single veteran stockbroker as “Yields hit 15-year high as bond investors damn ‘radical budget’”,

Savvy AFR readers might have been cognisant of a global bond market dive underway. Japanese 30-year bond yields hit their highest mark ever; US 30-year yields hit their highest since 2007; German 10-year yields were highest since 2011; UK and French 10-year yields highest since the GFC.

who knew Jim Chalmers’ budget would rattle the whole world?

For the record, the Australian 10-year bond yield was 5.04 per cent before the budget; it was down to 4.9 per cent by the end of last week.

Hat tip to the AFR’s Mark De Stefano for keeping perspective against the run of play, tweeting that the ASX 200 closed on 8670 before the budget and was 8670 ten days later.

So much for the end of capitalism Murdoch and Nine were promising.

Revolving doors of mediaCulture in any corporation is an interesting animal to read, but the first instinct is to self-replicate, “to hire people like us”. Smart boards and management try to neuter that instinct, but it’s difficult.

Back at the Nine board, Tonagh became chairman in November, just 10 months after joining the board. His predecessor was lawyer Catherine West, who joined the Nine board after 17 years at Murdoch’s UK Sky network, finishing there as director of legal and business affairs. West had, of course, taken over from Nine’s best-known chairman, Peter Costello. The AFR reported “she soon became a close ally of Costello” upon joining the board in 2016.

Aside from Tonagh’s Murdoch links, there are two non-independent directors representing the company’s biggest shareholder, conservative Bermuda-based tax exile Bruce Gordon.

Andrew Lancaster and Chris Halios-Lewis are respectively the CEO and CFO of Gordon’s WIN Corporation, Nine’s regional broadcasting affiliate, but also the company responsible for taking Murdoch’s Sky News from subscription to free-to-air television around the regions, doing for One Nation what Murdoch’s Fox did for Trump.

Independent director Mickie Rosen was an executive at Fox Interactive Media in the US.

Former accountant Timothy Longstaff was the Simon Birmingham staffer. He was also appointed by the Morrison Government to the Snowy Hydro board and the Takeovers Panel.

Which leaves Mandy Pattinson, formerly an executive with Discovery Communications, as the only director without a Murdoch or Liberal Party link on her CV.

None of the board has printer’s ink in their veins. (Tonagh’s rise to the top of News Corp was via Foxtel and REA.) Yes, Nine took over Fairfax. It wasn’t a merger.

Matt Stanton was promoted from CFO to Nine’s CEO in March last year. He has what the Nine website calls “strong experience as a commercial CEO” across food and beverage (Barambah Organics), retail (Woolworths) and media (magazines with Bauer and ACP).

Shares tumble, assets being soldIn short order, the new chairman and CEO have sold off Nine’s radio stations and regional TV and paid $850m to buy outdoor advertising company QMS from private equity firm Quadrant.

That price tag compares with the stock market’s valuation of $1.48B for all of Nine.

Nine shares were worth $2.37 upon taking over Fairfax eight years ago. They now trade in the lower 90 cents.

Nine could be worse, of course – it could be Seven, sliding away towards nothingness until taken over, sort of, by Southern Cross Media, which has a market capitalisation a third of Nine’s.

Or it could be 10, sent broke under Lachlan Murdoch’s leadership in 2017 and still allegedly loss-making, depending on how Paramount arranges its taxes in Australia.

And then there’s News Corp. Apparently, it doesn’t make a profit either, or so you might think given that it doesn’t pay tax.

It’s a bleak landscape, one where cultural similarities can be like holding hands, a dangerous thing lest it leads to dancing.

https://michaelwest.com.au/budget-hysteria-the-murdochification-of-nines-papers-in-full-swing/

PLEASE VISIT:

YOURDEMOCRACY.NET RECORDS HISTORY AS IT SHOULD BE — NOT AS THE WESTERN MEDIA WRONGLY REPORTS IT — SINCE 2005.

Gus Leonisky

POLITICAL CARTOONIST SINCE 1951.

RABID ATHEIST.

WELCOME TO THIS INSANE WORLD….

- By Gus Leonisky at 28 May 2026 - 6:55am

- Gus Leonisky's blog

- Login or register to post comments

fairer taxes.....

Michael Keating

Why the criticisms of Labor's tax changes are mostly wrongLabor’s tax policies will improve intergenerational equity and ensure more equal tax treatment of income from labour and capital.

Angus Taylor would like us to believe that Labor’s tax changes are anti-aspirational. These allegations merit an answer:

The capital gains tax and the incentive to innovate

At present 50 per cent of any capital gain is assessed for income tax, but Labor is proposing to return to the system originally introduced by the Hawke-Keating Government where all the real capital gain (after allowing for inflation) is subject to tax. These real capital gains are income and raise people’s purchasing power just as much as any other form of income. In fairness they should therefore be taxed at the same rate as any other income. Indeed, dividends from a company are taxed that way, and so should capital gains.

Nevertheless, it is argued by some that changing the capital gains tax will reduce innovation by new start-up businesses, in particular, for a start-up where the original value of the business was zero, meaning all the real gain will be subject to capital gains tax. The inference is that this will be a disincentive to start new enterprises.

There are, however, arrangements that allow small businesses with an aggregate turnover under $2m to significantly reduce, defer or disregard capital gains from the sale of active business assets. These arrangements are particularly directed at assisting people who are preparing for retirement, but even young entrepreneurs can defer all or part of their capital gains tax if they reinvest the proceeds into a replacement active business asset or use the funds to make capital improvements in an existing asset.

That still leaves the allegation that taxing real capital gains does not offer any offset for the effects of inflation on those new businesses whose assets start with a value of zero. It should, however, be possible to calculate the real gain by taking the present nominal value of the business assets and discounting that value by the rate of price inflation since the start of the business. And we know the proposed system of calculating capital gains did work from its original introduction in 1985 until 1999 when Howard and Costello replaced that system with the present 50 per cent discount.

Indeed, the evidence is that the rate of innovation was if anything better in that earlier period from 1985 to 1999, than since. Certainly, the rate of productivity growth was a lot higher in that earlier period, and productivity growth is the principal benefit from innovation.

There is, however, one difference between what the present government is proposing and the Hawke-Keating system of taxing real capital gains. In the 1985 model the gains could be averaged over five years to stop investors and start-ups being lifted into the top rate for that year. In that case, where the gains were averaged over five years, the taxpayer avoided being lifted into the top marginal rate as a one-off. If the Albanese Government wants to negotiate, then perhaps they should consider returning to this element of the 1985 model.

Another difference between the present capital gains tax proposal and the 1985 model is that the new tax will have a 30 per cent minimum floor on all real gains regardless of taxable income. Only taxpayers with a taxable income of less than $45,000 would be affected, and there are very few such taxpayers with capital gains who genuinely have such a low income. Instead, the intention behind this minimum tax floor is to eliminate the incentive to minimise tax by holding onto assets until retirement.

Are young savers disadvantaged?

Another criticism is that the changes to the capital gains tax will reduce the ability of young people, especially those working part-time and taxed at a lower rate, from saving for a housing deposit to build their wealth through shares. However, according to Tax Office data, only 4.4 per cent of taxpayers aged under 35 report capital gains: not many young people are saving by directly buying shares.

Furthermore, superannuation offers an alternative way for these young people to save a housing deposit. Superannuation savings are lightly taxed, and young people can access those savings years before they retire through the first home super saving scheme (FHSS). Under the FHSS, concessional contributions are taxed at only 15 per cent, which is usually less than the contributor’s marginal income tax rate. Assessable FHSS amounts also benefit from a 30 per cent FHSS tax offset. Contributions are limited to a maximum of $15,000 in any one financial year, and up to a maximum of $50,000 across all years. When the young first home buyer wants to pay a deposit on their first home they can withdraw up to 85 per cent of their concessional contributions to the FHSS. They will also be able to access an amount of associated earnings on both concessional and non-concessional contributions. In short, it seems unlikely young people will find it more difficult to save for a deposit on their first home.

The taxation of trusts

At present approximately 90 per cent of total private trust wealth is held by the wealthiest 10 per cent of households. Accordingly, the majority of trust income flows to the top-earning 10 per cent of families. The attraction of the trust is it allows income to be split among members of the family and thus lower the tax paid.

In order to improve fairness, the Government is introducing a 30 per cent minimum tax rate on discretionary trusts that will better align the tax rate on trust income with the tax rates paid by workers.

Notwithstanding self-interested complaints, this should not damage small business productivity. More than 90 per cent of all small businesses, including all farmers, will not be affected by these changes. Also, the changes only apply to new discretionary trusts, and the income from the assets of trusts existing at the time of the announcement will be excluded. While those businesses that will be affected could avoid the tax by changing their trust to a fixed trust or by incorporating their business. Starting from 1 July 2027 they will then have three years to do that.

The complainants are also calling the changes to the taxation of trusts the equivalent of death duties: these changes are nothing like death duties. Unlike death duties, the taxation of trusts is on income and not the capital value of the trust’s assets. And the changes to taxation of trust income is a move towards taxing that income at the same rate as the rest of us pay on the same income.

On an additional note, death duties are a good idea, and most advanced economies, including the UK and US, do have death duties, as Australia once did too. People who inherit have done nothing towards creating the wealth that they will inherit – otherwise it would be in their name at the outset. And fairness demands that those who inherit such wealth should share at least some of it with the rest of society.

Average tax rates

For a long time, a key part of the Coalition’s political message is that taxes will always be higher under Labor. A feature of Taylor’s budget reply speech was therefore that, if elected, a Coalition Government would restore tax indexation so that the average tax rate would not rise because of inflation.

While many will approve this change, which would stop taxation increasing by stealth due to inflation, in practical terms taxation in Australia is not high, and it is unlikely that indexation will lead to lower taxation than the Albanese Government is planning for in its budget.

In assessing taxation, our starting point should be to consider the purpose of taxation, which is to pay for the services that we want and need. Arguably many government services in Australia, such as health, education, aged care and defence, are presently underfunded. In addition, we are running too big a structural budget deficit.

An obvious indicator of how and why our services are under-funded is that compared to the other 37 countries in the OECD, Australia has the fifth lowest ratio of taxation to GDP. The only reason the US is lower is because it has a much bigger budget deficit. US government outlays are higher than in Australia, and the US is relying on the rest of the world to finance its living standards.

Some would say that we rely in Australia too heavily on income tax to pay for our government services. Even this is not true. For example, for a full-time Australian worker on an average wage their average tax rate is 23.5 per cent, which is less than the OECD average of 25.1 per cent. While for a dual-income Australian couple on average wages, with two children, their average tax rate is again 23.5 per cent, which is only slightly more than the comparable OECD average of 21.5 per cent.

Looking ahead, this Budget introduced a $250 tax offset for working Australians starting from 1 July 2027 and a $1,000 instant tax deduction instead of claiming expenses starting in 2026–27. According to Treasury modelling, this means the average tax rate for a worker on average earnings will actually be a little less in 2029–30 than when Labor was elected back in 2022.

In sum, the Coalition’s indexation policies are unlikely to make workers better off than under Labor’s tax policies.

https://johnmenadue.com/post/2026/05/why-the-criticisma-of-labors-tax-changes-are-mostly-wrong/

READ FROM TOP.

PLEASE VISIT:

YOURDEMOCRACY.NET RECORDS HISTORY AS IT SHOULD BE — NOT AS THE WESTERN MEDIA WRONGLY REPORTS IT — SINCE 2005.

Gus Leonisky

POLITICAL CARTOONIST SINCE 1951.

RABID ATHEIST.

WELCOME TO THIS INSANE WORLD….